The Real Math Behind Hardening A Wellington Storefront Against Wind

A Wellington storefront owner watched the building’s wind coverage jump past $6,000 a year while the rent barely moved. That gap is the whole story. The fix that actually lowers the number is impact window and door installation wellington fl, because hardened openings unlock the mitigation credits a landlord carries straight to the bottom line. Here is the thesis stated plainly: a commercial impact install lowers the total cost of carrying the building, not just the storm risk, and this piece runs the real numbers on a 3,000-square-foot retail unit.

Storefront Premiums Climbed Faster Than Rent

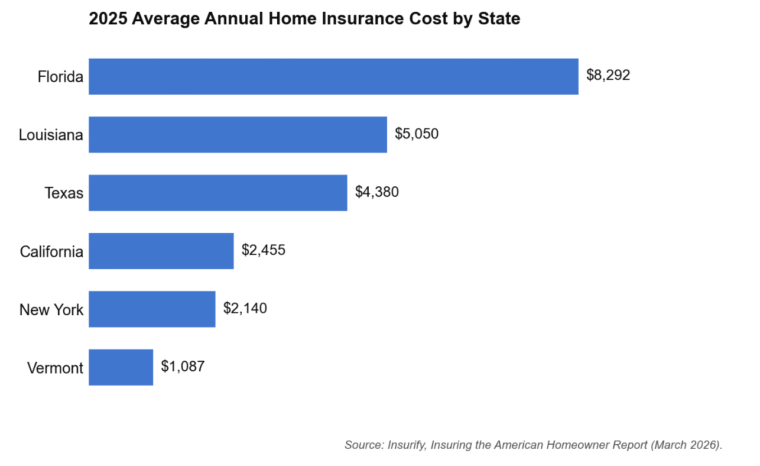

Commercial premiums in Palm Beach County have risen faster than almost every other line on the operating statement. The Insurify Insuring the American Homeowner Report published in March 2026 found that Florida premiums rose $1,252 in 2025 after roughly 300,000 Helene and Milton claims, and Citizens is now set to cut rates an average of 8.7%. Read that twice. One cut does not undo a decade of increases, and the case we see most often is an owner who budgeted for a three percent bump and got a number that cost him a full month of margin.

Ten years ago wind coverage on a small storefront was close to a rounding error. Now it ranks among the three biggest fixed costs on the building.

Wind Mitigation Credits Most Owners Miss

Florida carriers price wind risk off the openings first. Windows and doors are where pressure gets in and where a roof starts to peel, so a documented impact-rated opening is what actually earns the credit. The NOAA Office for Coastal Management puts Hurricane Milton at $34.3 billion in total costs, with 120 mph winds at landfall near Siesta Key on October 9, 2024, and losses on that scale are exactly what underwriters price into your renewal. Miss the credit and you pay for that risk twice, once in the premium every month and once when the storm finally arrives.

The mechanism is the wind-mitigation inspection. An inspector documents each opening’s rating and files it, and the carrier applies the discount tied to that report at renewal. The credit generally lands only once every opening on the elevation is covered, so a half-finished job leaves money on the table.

Pricing The Openings On A Retail Unit

A 3,000-square-foot retail unit usually carries one wide storefront system, a rear service door, and a couple of smaller openings. Say the storefront glazing runs $14,000, the impact entry door another $3,500, and the remaining openings bring it to about $19,000 installed. Those are illustrative figures for a tight-budget Wellington unit, not a quote you can hold me to. What matters is the order of magnitude, because that is the number you set against the premium line, month after month.

The storefront system is almost always the biggest single line, because a wide commercial opening needs heavier framing and larger impact glass than a house window. The rear and side openings cost less per unit but are easy to forget in a first bid. Get all of them onto one quote up front, or the number you budgeted drifts the moment the installer measures.

Financing Spreads The Cost Across Seasons

Few storefront owners write a $19,000 check in one shot, and they do not have to. JVR offers financing on commercial openings, which turns a lump sum into a monthly line you set against the premium credit. Reframe it: stop comparing the install to zero and compare the monthly payment to the premium dollars you already hand the carrier. Run it that way and the choice gets less dramatic.

There is a seasonal angle too. Wellington retail cash flow is not flat across the year, so lining the payment up against your slower months keeps the install from straining a tight budget. The install then competes month to month with what you already pay to insure the risk, which is the comparison that actually decides it.

Questions To Ask Before You Sign

Before you sign anything, make the installer prove the numbers you are counting on. Vague replies here are where budgets quietly slip. Ask these four and listen for specifics, not reassurance.

- Are these openings rated to the Florida Building Code approval my carrier wants? A good answer cites the specific product-approval number.

- Will you supply the wind-mitigation documentation my insurer needs for the credit? A good answer says yes and names the exact form.

- What is the total installed price with permits included? A good answer gives one out-the-door figure, not a per-window teaser.

- How long from deposit to final inspection? A good answer commits to a week range, not a vague season.

When The Payback Actually Arrives

Payback on impact openings is not instant, and anyone promising a two-year break-even is guessing. The honest range runs several years, driven mostly by how deep your mitigation credit lands and how fast Wellington premiums keep climbing, which is the one number nobody can pin down in advance. What holds up is the direction. A commercial impact window and door installation wellington fl owner completes today lowers the total cost of carrying the building every month it stands, credit plus lower energy bills plus the storm you never had to rebuild after. The spreadsheet doesn’t lie. Price the openings, ask for the mitigation paperwork, and weigh the monthly number against a premium that is not done climbing.