How to Get Out of Debt: Step by Step Guide to Feel Financial Freedom

What is financial freedom? Every person may have a different understanding of this subject. Some people may feel monetary free when they have enough means to pay for utility bills or cover a sudden auto repair while others dream of financial freedom to retire early or travel the world – learn more to find financial help.

You may have your own meaning of financial freedom but having debt is what makes you feel stressed about your present and future. And in the case when you think “I need money now” and immediately start searching for fast ways to get money – such a way of behavior is totally wrong on the path to financial freedom.

If you learn how to get out of debt and make savvy monetary decisions you will be able to control your finances and be prepared for minor uncertainties of life or unpredictable situations. Here is your guide to reaching financial freedom.

What Is Financial Freedom to You?

You can’t be financially independent when your finances control you or when you are deep in debt. You should learn how to repay existing debt and start living without it in order to gain control over your funds and manage them. This path may not be very easy but it’s definitely worth giving a try.

It won’t mean you won’t have any responsibility for your funds at all. Even when you get rid of the vicious debt cycle you will need to be accountable for your finances and how you handle them. Think of what financial independence means to you personally. Maybe it’s:

- Freedom to pay for utility bills or rent on time;

- Freedom to travel abroad;

- Freedom to establish an emergency fund;

- Freedom to set short- and long-term financial goals;

- Freedom to have enough cash in your savings account;

- Freedom to retire early.

Steps to Get Out of Debt and Become Financially Free

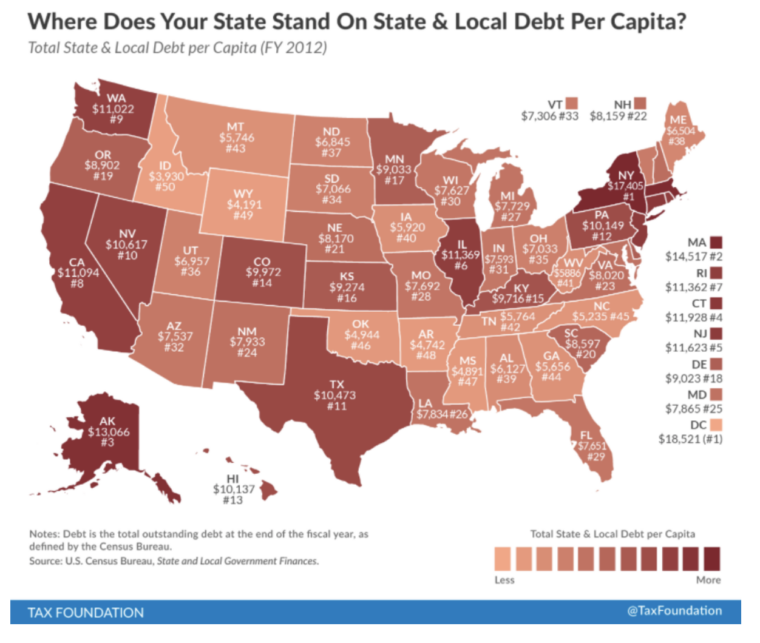

According to statistics, people with the highest average debt live in New York.

Below are the steps that may help to lead you to financial independence.

Step 1: Negotiate a Lower Rate

While you may have one or several credit cards, your aim is to repay the existing debt as soon as possible. Only when you break the endless debt cycle you will be able to start working your way toward becoming financially stable.

Why don’t you try to negotiate a lower interest rate with your creditors?

Maybe you’ve taken a small loan or a high-interest credit card before. You have the right to try the debt consolidation option or ask if you can qualify for a lower rate. You may need to make on-time monthly payments so that the lenders view you as a responsible borrower.

Step 2: Increase Your Debt Payments

If you can’t negotiate a better deal with your creditor you may want to increase the debt repayment percentage. If you start paying 15 percent of your monthly income or welfare benefits toward repaying the loan or the credit card, you will be able to become debt-free much faster.

The majority of credit card issuers ask borrowers to pay 2 percent of the monthly outstanding balance. If you keep on making small minimum payments your interest will keep on collecting. Repaying large amounts of debt each month will help you pay down existing debt much faster and avoid interest payments.

Step 3: Live Within Your Means

Your way to financial stability and independence may not be quick and simple. You should begin changing your daily habits and the way you live. Develop a different mindset and set financial goals you want to achieve.

If you decide to live within your means it doesn’t mean you will constantly live from paycheck to paycheck. It means you will have a chance to become wealthy and live a better life even if you’ve had debt in the past. The key strategy is to spend less than you earn each month and allocate more cash toward savings.

Step 4: Think of Your Career Choice

Did you have a chance to climb up the career ladder? Did you make a smart career choice? This question is essential when it comes to building your wealth and improving your financial wellbeing.

If you aren’t satisfied with your current position or you don’t earn enough to pay for necessities you’ve come to a dead end. It’s time to think about your present and what your future will look like.

Ask yourself where you want to be in ten or twenty years. Does your current job give you the potential for earning more? If you can’t grow and just live paycheck to paycheck you won’t reach financial freedom here. Make the necessary changes and opportunities where you can grow professionally.

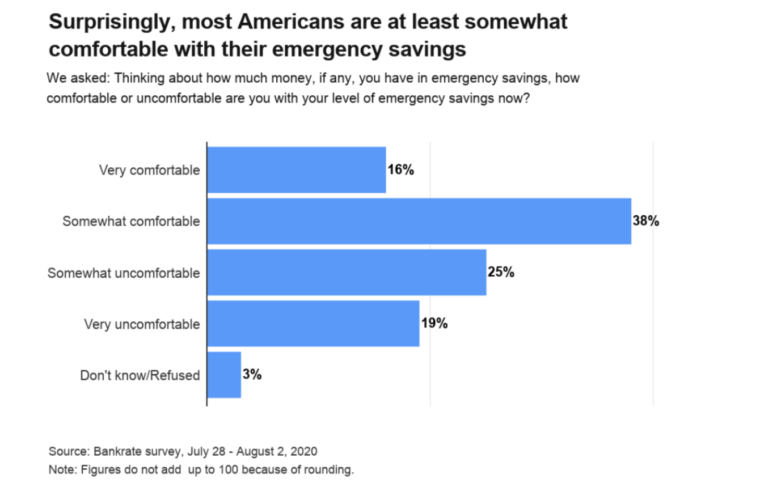

Step 5: Establish an Emergency Fund

You need to have an emergency fund so that it protects you in case of sudden financial shortfalls or money disruptions. Having an emergency fund differs from having a savings account.

Whereas a savings account is utilized for planned expenses, your emergency fund is meant to help you when an unforeseen cost appears. In other words, it will help you avoid taking out another loan or opening new credit cards as you will be able to use your own funds in case of an emergency.

Step 6: Monitor Your Credit

You may already know that having a good credit history allows you to qualify for better lending conditions. However, credit is also essential in many other situations.

For instance, when you land a new job the recruiter might check your credit history before he or she makes the hiring decision. Sometimes, insurance companies also utilize the credit history of the client to set policy premiums.

Knowing your current credit will help you understand what you may change to improve it. You can order a free annual credit report from one of the three credit reporting bureaus such as Experian, Equifax, or TransUnion.

STEP 7 : SEEK PROFESSIONAL HELP

Achieving financial independence is a goal many pursue, but unforeseen events or misjudgments can lead to daunting debt. Professional help, especially from debt relief programs, becomes invaluable during such predicaments. These programs offer tailored solutions, such as debt consolidation and negotiation. For Charlotte residents, for instance, various debt relief programs in North Carolina align with state norms and are just one online search away. Experts in this arena understand creditor tactics and legal debt nuances deeply. Their guidance helps individuals navigate financial hurdles, prevent errors, and ensure a route to fiscal stability. Without such expertise, many could overlook solutions or worsen their financial state. In essence, professional aid not only mitigates current strains but also preps individuals for sustained financial health.