Cons of Loans You Should Know Before Applying

The loan is a convenient financial tool that can help in a tough situation. But as with everything else in our life it has some downside you should consider. In this article, we plan to discuss the arguments against borrowing. It doesn’t mean that you shouldn’t apply. We just want you to make a fully informed decision.

Information is the key to success; that’s why it’s always advisable to raise financial literacy. Study all the information about personal loans online from PayDaySay what you need to know and apply the obtained knowledge to find the best terms and conditions for your situation. Some people are just not made for using the loans because of their personality; others have more beneficial alternatives. We’ll analyze the pros and cons of personal loans compared to other types of borrowing and give some recommendations.

Why Are Personal Loans Good?

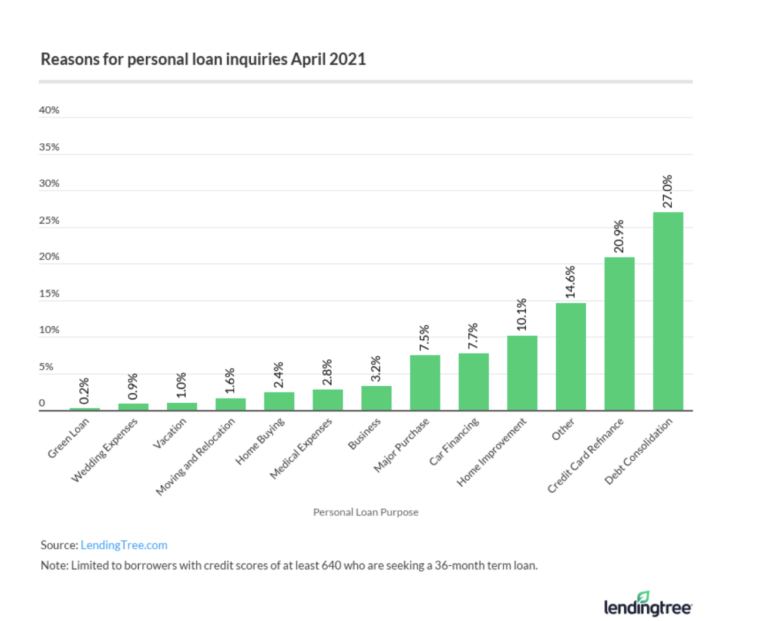

Do you know that last year 27% of personal loans were taken for debt consolidation? But ever more people took loans for car financing, purchases, home improving and credit card refinancing. It’s not just a current tendency because this kind of loan is designed for medium-sized purchases and other individual needs.

This positive aspect, actually, is a downside at the same time. The easy access to the money creates the illusion of their availability. Some people don’t even consider saving money for their wants because they can easily take a loan.

It’s a convenient method of closing a gap in a budget. The interest rates are usually quite comfortable, and the terms allow paying the sum back without a struggle. This loan type is not a good idea if you require money for business, but in most cases, lenders don’t limit the ways you can spend the funds.

These loans are easy to receive. Banks don’t require collateral, and the desired cash is available in a short time. In other words, with a decent credit score, you will highly likely receive the needed sum in a few days.

Reasons to Consider Before Applying

We described the positive sides of taking a loan; now it’s time to analyze the negative aspects. They can differ depending on your situation, but some downsides are common for all cases.

- Interest rates are higher than with other kinds of loans. Personal loans are relatively short-termed, so the lenders try to get the most out of them. As usual, the best conditions are offered for the best customers, so you are lucky if your credit score is higher than average. Collateral can lower the interest rates even more, but this option is possible only for certain loans.

- Fees and fines. Lenders take additional money to process the application, making personal loans even more expensive. Multiple lending organizations apply different penalties for borrowers. You may need to pay extra money in case of late payments or even with the early extinguishment of debt. Read the agreement carefully and pay attention to the details.

- Credit history. If you successfully pay the loan back, your score will only benefit from it. But don’t forget that lenders report all negative details of your financial behavior. Even one missed payment can be a disaster for your reputation.

- Debt increase. This point is true for any kind of loan, but in the case of personal borrowing, the debt is often unnecessary. It’s not like buying a new home, where you have no other choice apart from a mortgage. Stop for a moment and think, do you really need this car or flat TV. Maybe you can delay the purchase and save money for it instead of taking another loan.

- Risk for the property. If you decide to save some money on the interest rates and find a cheaper loan with collateral, you risk losing your possessions. In case of your failure to pay the debt in time, the lender will simply take the property you used for the collateralization.

When to Choose a Personal Loan?

We are not saying that this type of loan is pure evil. It has its own strong and weak sides. In what situations this kind of borrowing is the best choice?

- your credit history is good: with good credit, you have higher chances to receive beneficial offers from lenders;

- time is the essence: you need money really quickly and can’t wait for the approval too long;

- you plan to consolidate the debt: personal loans are a good alternative to the borrowings with higher interest rates;

- emergency: all the advantages of personal loans we mentioned previously make them a decent solution if you need to pay urgent bills or medical expenses.

If your situation fits into one or more parameters, go for the loan. Is it always so? No, some personality traits can cause you problems. We don’t recommend taking a personal loan, if:

- You have a tendency to spend more than necessary. Even if you pay the credit cards debt with the loan, you can easily create more debt the next month. If you are such a person, learn to control impulsive behavior first.

- Regular payments are a problem for you. If you don’t have a stable monthly income or have clear perspectives of losing your job in the nearest time, a personal loan is not for you. For this situation, the credit card can be a much better solution because of lower payments and the absence of a deadline.

- Money is not an urgent issue. If you can wait and save the money from your regular income, choose this variant. A personal loan is for really serious situations like an urgent car repair or a medical emergency. The bottom line is: don’t apply for a personal loan if you can comfortably do without it.

And the final recommendation, suitable for any type of borrowing. Before going to the financial institution, make a thorough plan of paying the loan back. Think through different possibilities. What option do you have in case of income reduction? How will you pay the debt if you lose the job? How will the monthly payments influence your everyday life and your family? Only with clear answers to these questions can you make an informed decision and make the most out of this financial tool.